Editor's Note: The following is a guest post written by Jon Wellinghoff and James Tong. Wellinghoff is the former chairman of the Federal Energy Regulatory Commission and is currently a partner at law firm Stoel Rives LLP. Tong is the vice president of strategy and government affairs for Clean Power Finance, a financial services and software firm in the residential solar market.

There’s a new point of contention between utilities and the solar industry: Should regulated utilities be allowed to rate base residential solar? That is, is the public’s interest best served by allowing a monopoly provider to invest in and own solar PV systems on people’s roofs and earn a regulated rate of return from all ratepayers? Rate basing solar is only part of a more fundamental question: To what extent should regulated utilities be able to profit from the impending boom in distributed energy resources (DER), many of which will be sited on customers’ properties and behind the meter?

Whether utilities should or should not be allowed to rate base DER may be a moot point. Rate basing residential solar or other DER might simply not be a smart business strategy for utilities. There are a number of challenges utilities will need to overcome to rate base solar.

Challenges to Rate Basing DG Solar

- The “Used and Useful” and “Prudent Investment” Standards: These are fundamental principles of utility regulation. Investments by regulated utilities must be used and useful to current ratepayers for the provision of utility service. Investments must also be prudently incurred to justify asking ratepayers to pay for them and their associated rates of return. Utilities’ historical obligation to serve includes planning for adequate resources to meet all customers’ needs. If utilities have planned appropriately, a “behind-the-meter” investment in DER probably cannot be justified, because prudent investments must be used and useful for all customers and not primarily for the customer who hosts the DER. Utilities can, however, potentially rate base DER that sit on the utilities’ side of the meter if they can meet the tests of prudency and being used and useful. Additionally, some states make specific statutory or regulatory exceptions to compensate utilities for promoting (but not rate basing) energy efficiency behind the meter. But these opportunities can be limited by other regulatory restrictions (see challenge #2). Further, utilities might have already disqualified themselves: by arguing that rooftop solar cannot be as cost-effective as centralized solar facilities, utilities themselves suggest that rate basing rooftop solar cannot meet the standards of prudent investment.[1]

- Anti-Trust Concerns: Governments have granted regulated monopoly utilities exclusive franchises along with exclusive privileges. These include: control of the distribution grid; access to customer data; regulatory imprimatur; captive ratepayers; and access to low-cost capital that comes from those captive ratepayers (to name a few). These privileges are intended to help utilities better serve the public, not discourage or engage in private competitive enterprise. Any attempt by utilities – perceived or real – to use these government-sanctioned advantages to compete against third parties will likely run afoul of anti-trust laws. Even the perception of competition from monopolies can stifle market entrants and innovations in DER and thus hurt the public welfare. [2] Utilities can also expect strong public backlash: witness the unlikely alliance between green and tea party activists, both of whom question the role of monopolies in DER sales.

- Lack of Expertise in Selling and Installing DER: Utilities with captive customers often lack the sales or marketing expertise to convince customers to adopt DER. Regulated utilities’ inability thus far to effectively use the 40 million smart meters already deployed strongly suggests that they may not be best able to leverage customer-sited DER. Similarly, utilities often lack expertise in installing DER or must rely on a more expensive labor force than those of third-party providers. Southern California Edison’s brief experiment with installing distributed commercial solar demonstrated that its labor force was not cost-competitive. If third parties sell and install DER more cost-effectively, it follows that regulated utilities cannot sell and install DER and still meet their legal obligation to provide the least-cost solution to ratepayers. Moreover, if utilities rate base DER and exceed their expected costs or underperform (as they have with smart meter deployment), who should bear the costs? Ratepayers or utility shareholders?

- Non Least-Cost Financing: Utilities are subject to normalization rules, which require utilities to spread tax credits associated with an asset investment over the life of that asset. [3] These rules do not apply to capital from competitive markets. This means competitive market capital can monetize tax credits faster, and then better pass the benefits on to customers. Additionally, equity capital from utilities can be higher than that in competitive markets. [4] (For those who need additional help understanding utility financing, we suggest reading our basic primer). The average authorized return on equity (ROE) for utilities is currently about 10%. Meanwhile, tax equity investors, who are largely financing residential solar, currently seek a lower, market-determined ROE of 7-8%. Unless utilities are willing to accept a lower authorized ROE (which seems unlikely) or partner with competitive players, rate basing solar and DER will not yield the least-cost option for ratepayers.

- Fiduciary Responsibility to Shareholders: The managers of investor-owned utilities (IOUs) are legally bound to serve the interest of their owner shareholders. Most shareholders invest in IOUs because of their low-risk profile, steady growth, and predictable dividends. Innovative technologies and business models, by definition, lack precedent and thus carry uncertainty. IOUs’ experimenting with them – much less competing against other players without having the appropriate competencies – will expose shareholders to risks they may not want to take. Deloitte writes: “A decision to transition to a higher overall risk profile will likely involve significant internal debate and the high probability of negative reactions from the financial markets and shareholders. This barrier may ultimately be deemed insurmountable—and as a consequence, new business model alternatives may be severely constrained.” Of course, utilities can try to use monopoly privileges to reduce these risks, but that takes us back to challenges 1 and 2.

- A Culture Focused on Conservatism and Cost: The regulated utility model is based on predictability. Shareholders expect predictable returns and utilities seek predictable revenue growth. Politicians and regulators demand reliable or predictable performance, and customers want predictable rates. Variability adds cost, and cost is an anathema to the prevailing model. Just look at the preoccupation with least-cost, fixed cost, cost-recovery, and cost-shifting. “Value” takes a backseat to “cost.” And even when “value” is considered, it is defined as “avoided cost.” After all, customers are ratepayers, and delivering value means keeping rates (i.e. costs) low. But greater deployment of DER won’t be predictable, and their value to customers will not be limited to avoided costs. DER will enable customers to spend less or do more – or do more and spend less. DER will increase reliability, resilience, control, and convenience. They will create new ways for customers to interact with energy and with each other, perhaps creating peer-to-peer models akin to those of Airbnb or Uber. To unlock the full potential of DER, prices cannot be narrowly defined by avoided cost; prices must be determined by customers’ willingness to buy and sell services. Regulated utilities have been struggling to convince customers of the value of the distribution grid. This suggests that utilities may not be qualified to capitalize on DER. If value is defined as avoided cost, it is unlikely that distribution utilities will be able to elevate the value of the grid in the customers’ mind; just to maintain the current performance of the grid, utilities will need to invest billions in the aging infrastructure and thus add more cost to end customers.

[1] This may not apply for all utilities. As Greentech Media reports, APS has been permitted (but not approved) to invest in rooftop solar after having stated that solar’s benefits are “unproven.”

[2] The Federal Trade Commission makes this argument in its filing in the New York’s REV proceeding.

[3] This ensures that future ratepayers benefit as much from tax credits as current ratepayers. However, the normalization rules only apply to rates charged to customers and not necessarily to taxes the utilities actually pay. A good discussion can be found here.

[4] Note: Having a captive ratepayer base gives a utility access to low-cost debt capital, which – when combined with their authorized ROE – can lower its total cost of capital relative to that of competitive market. Residential solar financing is mostly dependent on tax equity, but has been increasingly tapping debt capital through market instruments, such as securitization.

The Real Question: Where Will the Revenues Come From?

If regulated utilities already have trouble creating value for end customers, how will they pay for investment in the grid, much less investment in customer-sited DER? And if the answer to that question is unclear, we need to think seriously about how utilities might – or might not – profit from DER.

When businesses request capital for new ventures, the first thing capital providers look at is the revenue stream – how will new venture make money? The public needs to do the same with utilities, since ultimately the ratepayers will be paying for the capital if utilities rate base DER.

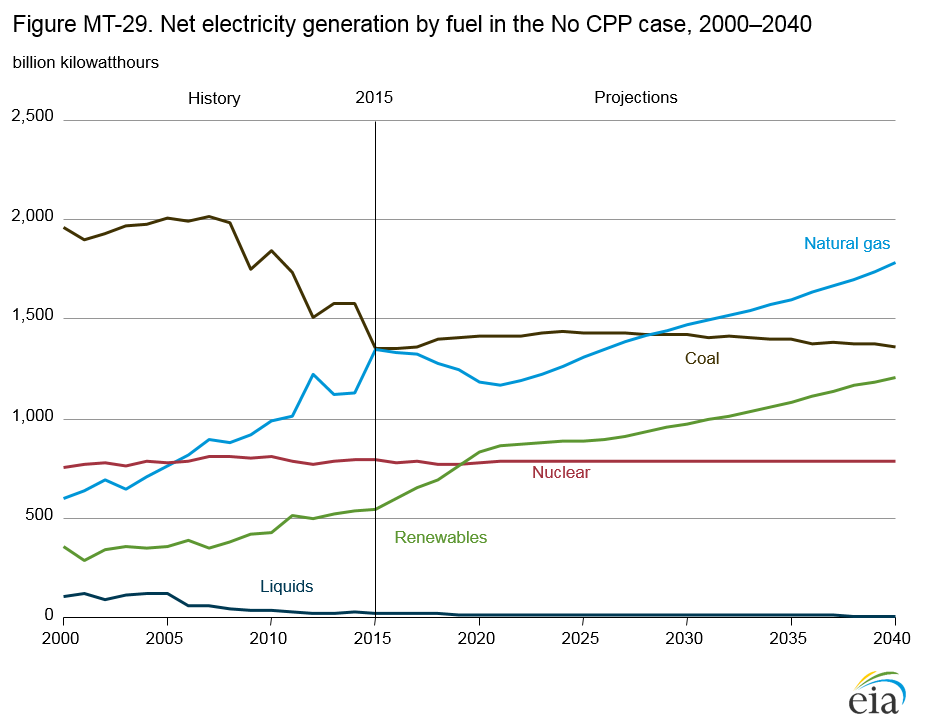

Utilities’ primary source of revenue is the sales of kWh. As the chart below indicates, that revenue stream has slowed to a trickle.

Rooftop solar serves roughly 0.5% of U.S. households – and most of that came online after 2007. Solar therefore cannot be the cause of this long-term decline in kWh sales. Increasing energy efficiency is the real “culprit.” Rate basing rooftop solar (or any DER) will not reverse this decline. In fact, more DER – even utility-owned – may depress the sales of kWh even further. Even worse, rate basing rooftop solar or other DER assets will only add to utilities’ fixed costs – the very problem utilities are attempting to solve by levying fixed charges on solar customers.

As we argued in a separate piece, the issue of “fairness” in rooftop solar is already convoluted. Rate basing rooftop solar only makes matters worse. Is it fair for utilities to incur more fixed costs by rate basing rooftop solar? Is it fair for them to demand that solar customers who got their solar elsewhere pay for those fixed costs, which include profits to utilities’ shareholders?

Conflating Recovery of Past Costs with Future Growth Opportunities

Utilities are indeed entitled to fair compensation for prudently incurred fixed or “sunk” costs. But there is no public obligation for regulated utilities to keep growing and sink more capital. As the Edison Electric Institute notes, “public utilities are, by extension, an arm of the legislature and, in turn, the people.” In other words, regulated utilities are quasi-governmental bodies. Like any government body, regulated utilities should only grow (or shrink) according to public needs.

If we accept that utilities exist to meet public needs, shouldn’t our primary concern be to determine what those public needs are? Rather than focusing on net metering and the “utility of the future,” we should be discussing future customer needs. And since we live in a free-market society, we must first ask how competition – not monopolies – could best meet those evolving needs. Only then can we determine the role of regulated utilities and their appropriate compensation.

Unfortunately, the utility vs. rooftop solar debate has completely flipped this logic. It presupposes that compensation for utilities is the top priority, followed by finding new profit opportunities for utilities. The role of markets and customer needs are almost afterthoughts.

A Solution to a Problem That Adds to the Problem?

But even by this distorted reasoning, rate basing solar cannot be justified. If utilities face increasing challenges in recovering costs for their current shareholders, why would they rate base DER and incur more obligations for future shareholders? Especially if those DER often reduce the kWh sales needed to pay current shareholders? Surely reducing utility obligations, not expanding them into untested business ventures, would be the most rational strategy? Deploying more capital to rate base DER only makes sense if those investments create new revenue sources. But what would those new revenue sources be?

Higher rates? But that would lead to the infamous utility “death spiral”. Increasing fixed charges? But as we argued previously, doing so is bad for the public and bad for the IOUs’ shareholders.

There may, however, be a new source of revenues that distribution utilities have largely overlooked.

The Utility Marketplace of the Future

The prevailing regulatory model considers safe, reliable, and affordable kWh to be the utilities’ “product.” The outlook for such a model is bleak. In this scenario, electricity is a commodity whose use is declining: the only way to increase customer value is to reduce cost. Even without the growth of DER, utility costs will go up; the aging infrastructure is already costing customers $18 billion to $33 billion per year in outages. But growth in kWh sales will remain flat, if not decline. The temptation to sell new products, such as DER, to end customers is understandable. But utilities may not be able to monetize those products precisely because of the challenges cited above.

The business case for regulated utilities to rate base customer-sited DER seems weak. The regulatory case may be even weaker. In rethinking their business models, utilities should also rethink where they can create value and then capture that value. Utilities would be far better off positioning the “grid” itself as their product. In that scenario, a utility’s main customers would be competitive third parties that want to plug into the grid and sell products or services to end consumers. Utilities’ revenue would come from entities that value the grid for its functionality, rather than its cost.

As we described in a separate piece, the grid can be a marketplace in which third parties and customer aggregators compete against each other to provide maximum-value DER to end customers. It would not be in the regulated utilities’ best interest to be a buyer or seller in such a marketplace. Doing so will discourage other buyers and sellers from entering and reduce the potential for strong “network externalities” that will increase the value of the grid. Additionally, competing in this marketplace will be riskier than traditional utility activities.

The optimal utility activity would not be to compete in the grid marketplace, but to host it. This would allow third parties to bear the risk of selling DER to end customers. Utilities could charge access or transaction fees for the value their assets provide to third parties – value that grows as more companies and people transact on the network. Utility revenues wouldn’t depend on the success or failure of any particular technology or company but rather on the success of multitudes of technologies and businesses using the grid – a far less risky revenue source.

For a robust network to take form, the distribution grid operator must be neutral. It must work objectively with the state commission to determine who makes what investments and how those investments would be best deployed, dispatched, and compensated. The grid operator’s incentives must be aligned with a reliable and efficient grid, and not biased by the interests of utilities’ managers and shareholders as well as the competing interests of third parties. We thus maintain that placing the functions and personnel associated with current grid operations into an independent distribution system operator (IDSO) will best serve the public, DER providers, and utilities.

What Business Are Utilities In?

Utilities have had trouble getting end-customers to understand the value of the grid. Maybe they should reconsider how they define their customers. Even without increasing DER deployment, the grid infrastructure will need tremendous upgrades. Higher costs and higher prices are inevitable. Monopoly providers that try to justify higher prices to current customers who have little understanding of the value of the grid will face an uphill battle. Why not instead sell the value of the grid to those who appreciate it – i.e., third party providers? Why not allow the IDSO to facilitate that new and fair marketplace?

Utilities need to ask themselves what business they’re in. If they’re in the business of clinging to monopolies, they’re heading for irrelevance. History hasn’t been kind to those who pursue this strategy. Ask U.S. Steel, DeBeers, or the original AT&T. If, however, they’re in the business of delivering innovative, value-added grid services, their future could not be brighter.

{kind=link}