New numbers show California’s peak demand will stress its grid more than previously thought, and in response policymakers are pushing ahead with an unexpected solution: electric vehicles.

In 2015, California’s grid needed as much as 10,091 MW of quick-responding resources to meet a three-hour load spike in the late afternoon and early evening. During the day, the state’s abundant rooftop solar keeps electricity demand flat, but it rises quickly as the sun sets each evening and residents return home from work.

As soon as 2019, that demand spike could be almost 14,000 MW, according to a recently-released report from analyst ScottMadden.

Using natural gas peaker plants to meet that load would impede the state’s plan to cut greenhouse gas emissions. And stationary storage, even with California's landmark storage mandate fully met, would provide insufficient ramping capacity. But electric vehicles (EVs) — already a benefit to utilities for the power demand they provide — could offer the grid something more.

If EV sales rise fast enough to meet Gov. Jerry Brown’s goal of putting 1.5 million zero emissions vehicles into service by 2025, EV battery storage could be an answer to the challenge of peak demand, according to a paper from California’s Alternative Fuel Vehicle regulatory proceeding.

“As net load decreases during midday and increases in the evening, the longer and steeper ramp up after sunset will require generators to respond quickly, according to the California Public Utilities Commission (CPUC) Vehicle-Grid Integration (VGI) white paper.

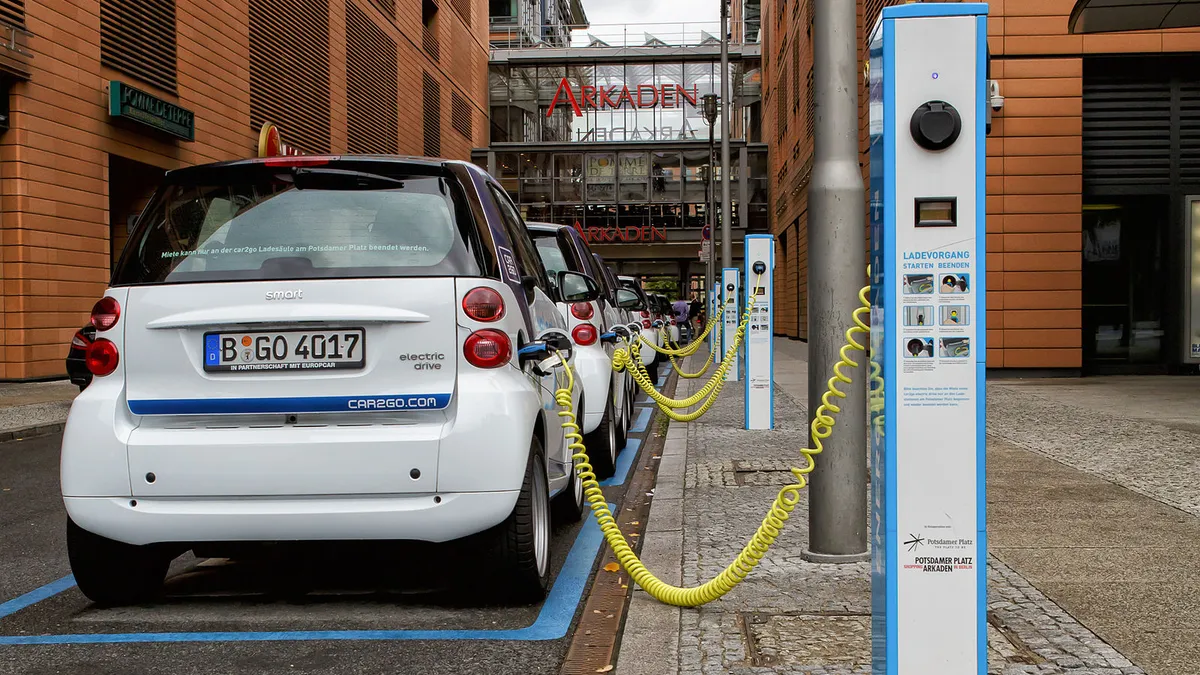

The EV batteries plugged into smart charging stations can be “fast acting resources” to meet grid needs, the CPUC paper reported in 2014. Those needs have been nicknamed the “duck curve” because a theoretical graph of them devised in 2011 looked like a duck, with the sharp, late-day ramp up in load as the neck.

The need to respond to that fast ramp is now more than theoretical. “The belly of the duck curve is much bigger, which means the ramp is steeper and that requires more fast ramping resources,” Swami Venkataraman, a senior vice president at Moody’s Investors Service, told Utility Dive on the sidelines at the recent Edison Electric Institute Financial Conference.

EVs plugged into smart charging stations are flexible load, especially with electricity price signals that influence when and how charging is done, Venkataraman said. “The utilities can use that flexibility instead of natural gas peaker plants to manage the duck better.”

By absorbing excess electricity in the middle of the day and reducing the amount of EV charging during the peak demand period, EVs can ease the pressure on the system by “making the size of the ramp smaller," echoed Chris Nelder, lead author of “Electric Vehicles as Distributed Energy Resources,” a recent paper from the Rocky Mountain Institute (RMI).

If California gets all the pieces in place, it could show how other states can use electric transport to integrate renewable energy with less fossil fuel use, added RMI senior associate Rachel Gold.

Such policies could increase the EV value proposition, boost sales, and increase the opportunity for private sector EV charging station providers. They would also be a new reason for utilities to support EVs and push to get into the business of building EV charging stations, presenting new questions of equity and fair competition for regulators across the country.

The EV need and opportunity

EVs integrated into the transmission-distribution system can be a resource that reduces costs for grid operators, the CPUC’s VGI paper reports. With properly structured policy, those cost savings could be returned to EV owners. The improved EV value proposition could drive transportation electrification and deliver more environmental and system benefits.

The California Independent System Operator raised concerns in 2013 that the conventional power system would be unable to accommodate the duck curve ramp in demand imposed by California’s very large solar penetration.

Without more flexibility, solar penetrations as low as 20% could require curtailment of 30% of the state’s solar generation, potentially eliminating its cost-effectiveness and putting California’s 50% renewables mandate out of reach. But grid-integrated distributed energy resources (DER), including distributed solar, battery storage, and EVs would “allow maximum use of the solar resource.”

The ScottMadden research shows the challenge has become bigger since 2013. Reseachers found the maximum three-hour ramp was 6,245 MW in 2011, 8,049 MW in 2013, and 10,091 MW in 2015. That is an average maximum ramp increase of 962 MW per year.

Without considering solar growth or technology and market changes that could alter the trajectory of solar adoption, the annual maximum ramp in 2018 would be 12,977 MW and in 2019 it would be 13,939 MW, according to ScottMadden.

The worsening duck curve would be driven largely by utility-scale solar growth, increase ramps throughout the year, and would be most severe on the weekends, the researchers reported.

Even without the potential system impacts from EVs, their deployment offers a huge opportunity, particularly for utilities, Venkataraman said.

If California gets to its target, EVs will account for over 50% of annual electricity sales growth in the state by 2025 and two-thirds of annual growth by 2030. By 2030, he said, EVs would be 5% of all electricity sales in 2030.

Moody’s assumed non-EV load would grow at 0.5% per year in the same period, but if it remains at the even lower growth rate utilities have seen in recent years, “EV-related load will only be more important for the sector,” the paper points out.

As a significant driver of load growth, the EV market would expand opportunity for both independent power producers (IPP) and utilities, Moody’s argues.

“IPPs face weak cash flows in California due to low natural gas and power prices and a glut of renewables,” Moody’s reports. “Anemic power demand growth also contributes to the challenged outlook.”

California’s big three investor owned utilities — Pacific Gas & Electric (PG&E), Southern California Edison (SCE), and San Diego Gas and Electric (SDG&E) — “are much less sensitive to power volumes owing to the presence of a decoupling mechanism,” Moody’s adds. But “there is substantial ongoing capex in the grid independent of EVs (PG&E and SCE are each spending over $5 billion annually).”

This benefit would allow utilities “to spread these costs over growing sales volumes…[and] mitigate tariff increases for customers,” Moody’s reports.

The bargain will not be as good for the Los Angeles Department of Water and Power (LADWP) and a handful of other municipal utilities in California, Venkataraman said. Unlike the state’s three dominant investor-owned electric utilities (IOUs), some munis are reconfiguring generation portfolios with as much as 40% coal, but do not want to take on any more capital expenditure than is necessary.

“To reduce coal cost-effectively, LADWP wants to decrease load, so if EVs increase load, it makes the transition more difficult and expensive,” Venkatamaran said. “They will probably have to invest in more renewable energy and natural gas infrastructure.”

There could also be enormous emissions reductions and health benefits if California gets to its ZEV target, Moody’s reports. “By 2030, emission reductions could be 12% annually and cumulatively worth $725 million.”

The significant reduction of non-CO2 pollution as a result of cutting carbon emissions could reduce the state’s health insurance costs by $200 million or more, Venkataraman said.

“Cleaner air will also improve productivity and quality of life over the long-term, increasing the state's in-migration and boosting the economy,” Moody’s adds.

The transition to electrification could cost California $3 billion in gas tax revenues by 2030 but that is less than 3% of the state’s annual $114 billion budget and can be offset in the normal budget-making process, Venkataraman said.

Moody’s study of California’s EV market was prompted by the fact that the state is half the U.S. EV market and a quarter of the global EV market, Venkataraman said. The policy work being done in the CPUC’s Alternative Fuel Vehicle docket to get the state to 1.5 million ZEVs by 2025 could be a template for other states.

“Future duck curve sightings may well occur sooner than we think in states with growing utility-scale solar, such as Arizona, Georgia, Nevada, North Carolina, or Texas,” the ScottMadden paper observes.

To reach its EV penetration target, annual new vehicle sales in California would have to go from 2015’s 3% to 15% in 2025, Moody’s reports. That is a growth rate of 18% per year through 2020 and a 25% per year growth rate from 2021 to 2025.

But California cannot just mandate the deployment of EVs the way it has mandated renewables and battery storage. “Customers have to buy the cars,” Venkataraman said, “and, at present, both the price and the lack of charging infrastructure are impediments,”

California has already put dozens of financial and other policy incentives in place to drive growth, he said. It adds rebates of $1,500 to $2,500 for various EV models to the $7500 federal EV tax credit.

It also has a competitive grant program that provides $100 million per year for transportation and fuel technology innovations and the buildout of EV charging stations. In addition, the three IOUs may be authorized to invest a cumulative $1 billion in building charging station networks in their service territories.

But at the present rate of growth of approximately 200,000 ZEVs per five years, California may not have more than 600,000 ZEVs in 2025. That is why the CPUC has called for new workshops on vehicle deployment and charger buildout in December.

It is also why RMI researchers asked how regulators can think more effectively about policies to drive EV growth.

Key policy questions

Signs of an EV revolution are appearing, said RMI’s Gold, co-author of “Driving Integration; Regulatory Responses To Electric Vehicle Growth,” another RMI paper.

Over 20 plug-in vehicle models are now or will soon be available. Battery costs have fallen 70% in recent decades and continue to decline. The number of charging stations has grown 40 times over in the last eight years.

But the proliferation of the technology means regulators and electric utilities must “account for the emergence of a new industry paradigm that challenges traditional policy frameworks,” the RMI paper notes. Regulators and policymakers must “ensure EVs benefit ratepayers, utilities, and the grid.”

The paper on policy, Gold told Utility Dive “is to help regulators think through their role.”

There is no single policy or approach that will streamline growth and “allow EVs to be smart load instead of dumb load,” Gold added. “Some regulators are being proactive and understand the potential and others have state lawmakers telling them to take a role.”

RMI’s paper identifies and explores six core questions in three categories that regulators can use as analytical tools, Gold said. With the tools, regulators can develop rate designs and complementary policies for the kind of EV growth they want in their states.

Regulatory roles

The first category is about utility regulators’ roles and what criteria regulators should use to decide whether EV deployment is in the public interest, Gold said.

The extent of regulators’ roles will vary, RMI observes. They can be more proactive where it is clear integrating EVs meets their core responsibilities to minimize costs to ratepayers and ensure safe, reliable service and infrastructure at just and reasonable rates.

Regulators also should recognize that unmanaged charging at relatively low levels of penetration can stimulate EV markets, but higher penetrations may require intervention if those same core responsibilities are to be fulfilled, RMI adds.

There are two kinds of competing public interests that must be balanced, RMI observes. The interests of both ratepayers and EV owners are involved in rate design, in utility ownership of EV charger infrastructure, and in siting chargers. In deciding between them, regulators should consider what is best for the grid as a whole.

EV siting and aggregation

The second category of questions is about how to set rates and make rules to guide the siting of charging infrastructure and the aggregation of EV batteries as a market resource, Gold said.

Smart siting of charger infrastructure can maximize the value of EV batteries as demand response (DR), RMI reports. It begins with utility planning. In the best locations, a balance of “grid system-oriented rates” and “customer-oriented rates” can be used to encourage charging that reduces the size of the midday load drop-off and the size of the system peak.

Tension can emerge between the two types of rates if the ones that offer incentives to charge at times and in locations best for the grid are not the most customer-friendly rates, Gold said.

There is little known about the design of market rules because aggregated DER cannot be a DR product or an ancillary service product in most markets, Gold said. “Rules that require a certain scale or availability at certain times might prevent EVs from participating.”

In reviewing market rules and the technical and legal barriers to entry that aggregators of DER face, regulators can focus on balancing the needs of market participants and system operators, RMI suggests.

Utility ownership of EV charging infrastructure, discussed below, is also in this second category of questions.

Rates and pilots

The third category raises the more abstract question of how regulators can make the policies and rates they put in place adaptive, Gold said. “This is a new, high-tech, fast-changing market but utility regulators work in decades-long time frames and don’t change quickly.”

Customers have tended not to respond to new electric rate designs but seem to respond strongly to fluctuations in gasoline’s pump price, Gold said. “This is a merging of those two markets and we don’t know how people will respond.”

A key solution is “scalable demonstration projects to test EV integration approaches and allow solutions to evolve iteratively,” RMI argues. Such pilots could allow stakeholders to collaborate, experiment, scale, and measure success with clear metrics, the paper adds.

Another possibility is to include more stakeholders in tests of new rate designs and new methods of distribution grid planning.The objective would be to learn “things that are now unknown,” Gold said. “This is the human part of policy and humans are unpredictable and we need regulators to be adaptive to that.”

Utility ownership of charging infrastructure

It is not clear whether utilities, private sector providers, public entities, or some combination of the three would best speed the deployment of EV charging infrastructure, the RMI paper reports.

Utilities and public entities are useful for deploying an initial network of chargers, as they can put them in places that would initially not provide enough income from customer charging to earn a profit. But private charging companies worry these entities could monopolize the market, and consumer advocates raise concerns about the cost-effectiveness of charger investments.

“Regulators must determine the extent to which the ‘regulatory compact’ with monopoly utilities should be extended to ownership of EV charging infrastructure,” Moody’s points out.

There is little doubt the growth of EVs provides utilities with a big capex opportunity.

“Originally, PG&E, SCE and SDG&E proposed EV infrastructure programs to build up to 62,000 charging stations at a total cost of $1.1 billion,” Moody’s reports.

The CPUC subsequently limited the IOUs to Phase I pilot programs. SDG&E will invest about $100 million in 3,500 charging stations and SCE will spend $22 million on a third-party owned buildout of about 1,500 stations. PG&E’s pending $130 million, 7,500-station proposal will include both utility-owned and third-party owned chargers.

The first regulatory question is whether utility ownership is an intrusion into the private sector. The second is whether the benefits to ratepayers from utility ownership are more important than the abridging of the regulatory compact. Many EV advocates say they are.

“ChargePoint, which owns 70% of California’s charging stations, Tesla, Greenlots, and NRG subsidiary EVGo are the major providers,” Venkataraman said. “They are all essentially start-ups. A CPUC-approved utility plan offers certainty those companies cannot that mitigates some of the risk of EV ownership.”

Utility ownership would overcome the chicken-and-egg conundrum and get urgently needed charging infrastructure in place, Venkataraman added. But it would not saturate the market and, in the long term, there could be a substantial private market.

RMI’s Gold sees other nuances in the question. “The reasons for utilities to own charging infrastructure relate to their existing customer relationships, their knowledge of the grid, and their ability to finance high capital cost infrastructure,” she said.

Private provider advantages include the pricing efficiency of competitive procurement and the ability to scale beyond limited service territories, she added.

It is possible both could have a role, she said. If EV deployment is to be done in both an economic and an equitable way, utilities might address the un- or underserved segments of the market that private companies to not reach.

The best example might be the split incentives associated with charging infrastructure for multifamily buildings, Gold said. “The people who would benefit from having chargers are not the building owners who would be the ones who would install the infrastructure. That is a potential market failure that could be an opportunity for a municipality, a utility, or a community choice aggregator.”

That market failure is one of many diverse opportunities utilities could take advantage of to serve customers, build load, and meet their service obligations, Gold said. “It is also a wakeup call for regulators to begin to help utilities figure out where EVs will be on their distribution grids, what kinds of rate designs will be necessary, and how to be more adaptive.”